MODEL ANSWER PAPER

UNIT- 1

Q. 1. Critically explain the wealth definition of economics?

The wealth definition is the fundamental definition of economics. The economics is derived from the Greek word oikos and Nomos which means household and management .So in its original sense, economics means house hold management that is satisfying as many wants of the family as possible by economizing or wisely allocating the limited resources at the disposable of the family among different wants or uses. it may be noted that Aristotle the famous Greek philosopher considered economics as the art of household management.

Today the art of household management is provided by everybody that is; govt. as well as individuals. For the management or solution of the day to day economics problem, arising from unlimited wants and limited resources by economizing or distributing wisely the limited resources among different use. In other word economics is a study of how many uses his limited resources wisely and satisfies as many wants as possible. In short economics is the science that studies how human beings try to satisfy their unlimited wants with limited means or resources.

Definition of Economics:

Definition of economics means the description of the nature of economics. In short, it means the meaning of economics. The object of defining economics is to point out what economics is and what it is not.

There are many definitions of economics. But they are classified into four groups they are.

- Classical or wealth definition

- Neo-classical or welfare definition

- Scarcity definition

- Modern or growth- oriented definition

WEALTH DEFINITION

Adam Smith the father of Economics gave the wealth definition of Economics which is also called as classical definition of Economics. He defined Economics in his famous book called an enquiry in to the nature and causes of wealth of nation in 1776 which popularly known as wealth of nation .He said economics is a science which studies the nature and causes of wealth.

The followers of Adam Smith were J.B Say, J.S Mill, N.W Senior, F.A Walker etc. In the view of these economists accumulation of wealth is the main aim of economic activity such as Production, Distribution and Exchange.

CHARACTERISTICS OF WEALTH DEFINITION

- The study of wealth is Economics which deals with production, exchange and distribution of wealth.

- Only material goods or commodities are considered as wealth which are scarce and useful. Non material goods, services and the goods which is freely available in the nature are not wealth according to wealth definition.

- According to wealth definition economics studies the causes of wealth which brings economic development. Adam smith supports that, to increase wealth production, the production of material goods will have be increased. This can be done with the help of division of labour, increase in demand, investment and of course with free economy.

CRITICISM OF WEALTH DEFINITION

The wealth definition came in for severe criticism from literary men and social reformers like Thomas Carlyle, John Ruskin, and Mathew Arnold Dickson etc. The criticism is as follows.

- Much importance given to wealth: Wealth has been given much importance in economics. So Carlyle stated economics as pig philosophy, because it is supported acquisition of wealth.

- Absence of man’s Welfare: The wealth definition has not given any importance to the economic welfare of the society. It gives importance only to the accumulation of wealth.

- No mention of means: This definition makes the earnings or accumulation of wealth is an end itself. It does not tell about the purpose of means of earning wealth.

- The meaning of wealth was restricted: According to wealth definition material goods only are considered as wealth, but modern economists used the word wealth for both goods and services. Thus the meaning and scope of wealth was restricted.

Q. 2. What is Socialism? Explain the merits and demerits of Socialism. 10- MARKS

Socialism is also called as planned economic system. It is an economic organization of society in which the material means of production or own by the whole community and operated by organs representative of and responsible to the community. According to a general economic plan all member of the community being entitle to benefits, from the result of such socialized planned production on the basis of equal rights. The merits and demerits of socialism explains the nature of socialism promptly.

Merits of socialism:

- Social Justice: The goal of socialism is social justice under socialism the inequalities of income are reducing to the minimum and the national income is equitably distributed.

- Economic use of resources: The production resources of the nation are more economically and optimally allocating among the various productive uses.

- Full employment: Under socialism social ownership of factors of production an adoption of central economic planning enables the main importance of full employment.

- Economics stability: Socialism ensures economic stability by eliminating trade cycles through the control of state on production.

- Stability of price: The prices are fixed by the authority but not by the demand and supply forces as per market mechanism and hence prices remains stable

- Production of goods according to social priorities: Goods are produced according to social priority and not on the basis of maximization of private personal profit.

- No exploitation: In socialism there is no class of employers exploiting workers. Under social ownership, workers are in a sense of co-owners of the factories and firms where they’re working.

Demerits of socialism:

- Concentration of power in the state: The greatest danger of socialism is that too much power is concentrated in the state.

- Loss of personal liberty: There is no scope to the individual to speak or to behave with Liberty or show his ability of entrepreneurship. The free choice of occupation will go with the assignment of jobs.

- Lack of incentives: Incentive to hand work and stimulates to self-improvement disappear altogether when personal gain or self-interest is eliminated.

- Actions of effective competition: Under socialism there is absence of effective competition both among persons and among enterprise.

- Loss of consumer sovereignty: Under socialism, consumers have to adjust to production. Quota and rations are common he will not be able to maximize is satisfaction.

- Red tapes: There will be Red tape and the bureaucrats cannot take quick decision in running of the economic machinery.

- In efficient running of business: The condition in government service or not congenial for the display of extraordinary ability and a government department cannot claim success in business.

- No economic equality: There is still difference in income of the person and there are poor and rich even under socialism.

- Insufficiency of resources: The resources often maybe allotted to industrial which are less profit-making units due to the social priorities. Government cannot raise the huge amount of capital which is the basis of economic development.

- No rational in pricing system: Under socialism prices do not reflect factor cost.

SHORT NOTES:

- CONSUMPTION:

In ordinary language, the term consumption means eating some food stuffs but in economics, Consumption refers to the use of goods and services by individuals or households to satisfy their wants and needs. In the context of economics, consumption is a crucial component of the overall economic activity. It involves the purchase and use of goods and services, ranging from basic necessities like food and shelter to luxury items and services. The Importance, features are economic growth, employment etc.

Importance of Consumption:

- Economic Growth: Consumption is a significant driver of economic growth. Increased consumer spending stimulates demand for goods and services, leading to higher production, job creation, and overall economic activity.

- Employment: Consumer spending creates demand for goods and services, which, in turn, encourages businesses to produce more. This increased production often leads to the creation of jobs, contributing to lower unemployment rates.

- Business Profitability: Businesses depend on consumer spending for their revenue. When consumers are willing to spend, businesses can thrive, invest in expansion, and generate profits.

- Standard of Living: Consumption is directly tied to the standard of living. Higher levels of consumption can lead to an improved standard of living as individuals and households have access to a wider range of goods and services.

- Investment Incentives: A healthy level of consumption can create a positive economic environment, encouraging businesses to invest in new technologies, research and development, and other innovations.

- Market Signals: Consumption patterns provide valuable information about consumer preferences and market trends. Businesses use this information to adapt their strategies and develop products that cater to consumer demands.

Types of Consumption:

- Durable Goods Consumption: Involves the purchase of goods that are expected to last for an extended period, such as cars, appliances, and furniture.

- Non-durable Goods Consumption: Involves the purchase of goods that are consumed quickly and have a short lifespan, such as food, toiletries, and clothing.

- Services Consumption: Encompasses the purchase of services rather than tangible goods. This includes things like healthcare, education, entertainment, and professional services.

- Necessity Consumption: Involves spending on essential goods and services necessary for daily living, such as food, housing, and basic healthcare.

- Luxury Consumption: Involves spending on non-essential, high-end goods and services that provide comfort or pleasure, such as designer clothing, fine dining, and luxury vacations.

- Direct or Final Consumption: When commodities and services are directly used to satisfy the wants of consumers, it is called direct consumption. Eg. Food, clothes, books, furniture, radio etc.

- Indirect or Productive Consumption: When goods and services are indirectly used to satisfy the wants of consumers, it is called as indirect consumption. Eg. Raw cotton, jute, sugarcane etc.

2. GOOD:

In ordinary usage, only tangible or material thing, such as books, furniture, clothes, food etc. are called good. But in economics, a “good” refers to a tangible, intangible item that satisfies human wants and needs. Goods can be physical objects, such as cars, clothing, and food (tangible goods), or they can be services, such as education, healthcare, and entertainment (intangible goods). Goods are essentially products that have economic value and are exchanged in the marketplace. The classification of Good is a very interesting topic here.

Classification of Goods:

- Free Goods: Those goods which do not command price like gifts of nature, Eg. Air, water, sunshine etc. are examples of free goods.

- Economic Goods: Goods which have utility and which are scarce in supply like food, clothes, books furniture, machine, etc. are called economic goods.

- Consumer or Consumption goods: These goods are those which are used for final consumption.. They satisfy the wants of consumer directly. Eg. Food clothes, sugar, toothpaste, soap etc.

- Capital goods or Producer goods: Goods which are used in production of other goods either consumer goods or producer goods are called capital goods. Eg. Machines, tools, buildings. Etc.

- Intermediate goods: The goods which lie in between consumer goods and capital goods are called as intermediate goods. E.g. processed raw materials.

- Private Goods: The goods which are owned and consumed exclusively by an individual are called private goods. e.g., a book, a car, TV, Scooter, Car etc.

- Public Goods: Goods which are owned and consumed by society as a whole are called public goods, such as national defense or public street lighting, public parks, cinema halls, public hospitals etc.

- Common Goods: Non-excludable but rivalrous, such as fish in the ocean or pastureland.

- Durable Goods: Goods with a longer lifespan, like appliances, furniture, and vehicles are called durable goods.

- Non-durable Goods: Goods that are consumed relatively quickly, such as food, beverages, and toiletries are called non-durable or perishable goods.

- Tangible Goods: Physical products that can be touched and seen, like clothing, electronics, and machinery are tangible goods.

- Intangible Goods: Non-physical products or services, such as education, healthcare, and software are called intangible goods.

IMPORTANCE OF GOODS

Goods play a important role in economics as they are tangible items that satisfy human wants and needs. The importance of goods in economics can be understood from various perspectives:

- Utility and Satisfaction: Goods are produced and consumed because they provide utility, which refers to the satisfaction or pleasure derived from consuming them. Different goods offer different levels of utility to individuals.

- Factors of Production: Goods are one of the final outcomes of the production process, which involves the combination of factors of production such as land, labor, capital, and entrepreneurship. The production and exchange of goods drive economic activity.

- Exchange and Trade: Goods are exchanged through markets, and trade is a fundamental aspect of economics. The exchange of goods allows for specialization and comparative advantage, leading to increased efficiency in resource allocation and production.

- Economic Growth: The production and consumption of goods contribute to economic growth. Increased production of goods can lead to higher GDP, employment, and overall economic development.

- Income Generation: The production and sale of goods generate income for individuals and businesses. This income, in turn, contributes to household budgets, business profits, and government revenue through taxation.

UNIT- 2

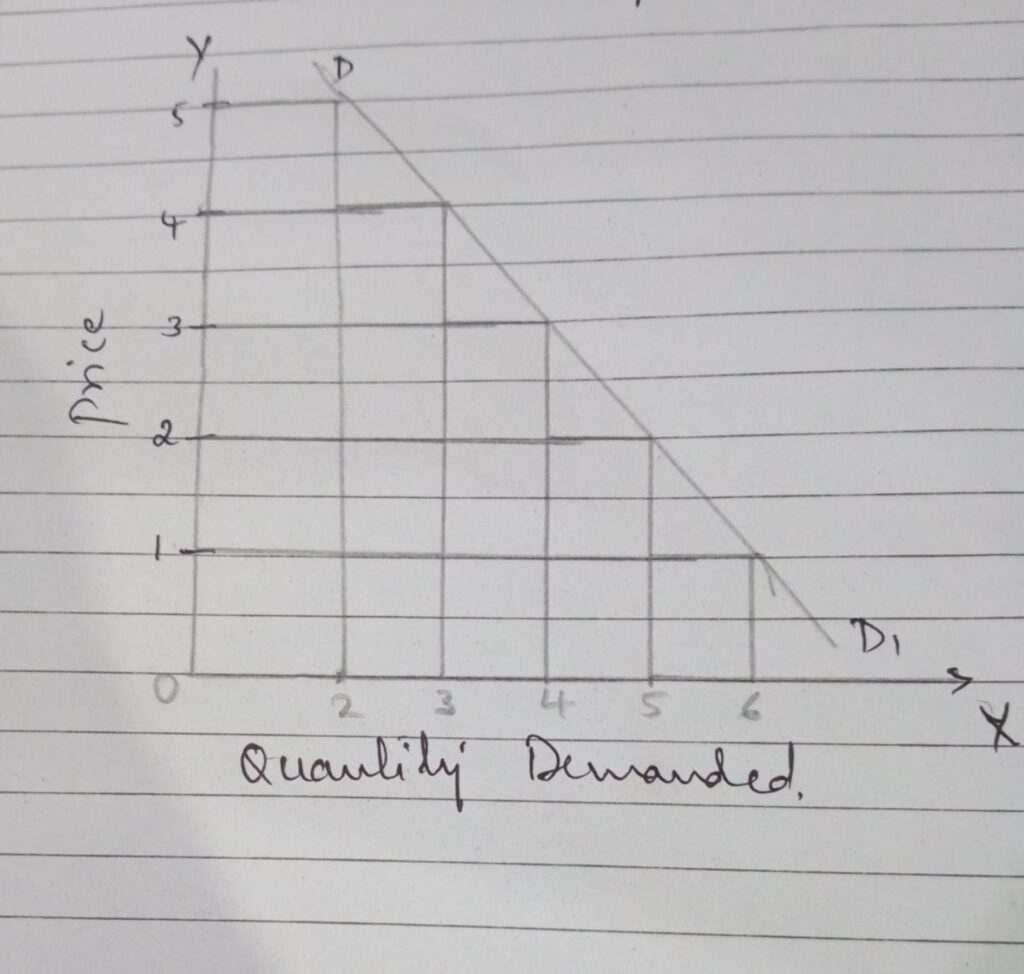

Q. 1. Explain the Law of demand with the help of schedule and diagram.

The law of demand holds a great importance in economics, before this meaning of demand we learn. The term demand is different from desire, want; wish etc. In economics the term demand has different meaning. Any want or desire will not constitute demand. Demand is not mere desire for a commodity but it is the effectiveness desire for a commodity. It means desire plus willingness and capacity of a consumer towards commodity. Demand refers to the total quantity of a commodity that are purchased by a consumer in the market at a particular price at a particular time. The law of demand depends on various aspects.

Features of the law of demand:

- Inverse relationship: There is an inverse relationship between price and demand

- Price is an independent variable and demand is a dependent variable: in this case we study the effect of price on quantity demanded only.

- Quality statement: It tells us only the direction of change in price and demand but does not indicate the quantity changes in both price and demand.

- Qualifying phrase: The operation of law is condition by the phrase other things being equal it indicates that a law does not have universal application, it indicates only the general tendency of buyers

- Negative slope of the curve: Generally demand curve sloped downward from left to right.

Law of demand:

The law of demand explains the relationship between price and quantity demanded of a commodity. it indicates that demand varies inversely with the price, the law can explain in the following manner, “other things being equal a fall in price leads to expansion in the demand and rise in price leads to contraction in demand” in the words of Bilas, the law of demand states that other things being equal quantity demanded per unit of time will be great, the lower the price and smaller, the higher the price. The law can be expressed in mathematical term as “demand is a decreasing function of a price symbolically D=f(P) where D represent demand P stands for price and F denotes of functional relationship. the law explain the cause and effect relationship between independent variable f and dependent variable P there is no rule that a consumer have to buy more whenever price falls and vice versa. The law explains only the general tendency of consumers while buying a product it does not have universal validity. It is conditional in nature.

The law of demand can be explained with the help of demand schedule the demand schedule explain the functional relation between price quantity variation. it is a list of various amount of a commodity that a consumer is willing to buy at a different price at one instant of time. the following individual demand schedule shows that people buy more when price is low and buy less when prices are high.

| Price in rupees | Quantity demanded in unit |

| 5 | 2 |

| 4 | 3 |

| 3 | 4 |

| 2 | 5 |

| 1 | 6 |

It represents the functional relationship between quantity demanded and price of a given commodity. Generally the demand curve has a negative slope or it slope downwards to the right. The negative slope of the demand curve clearly indicates that quantity demanded goes on increasing as price falls and vice versa.

Assumption of the law:

- Taste and preference customs and habits of consumer should remain constant

- Price of related good should not undergo changes

- Income of the consumer should remain the same

- No substitute would be discover

- Consumer should be anticipate change in prices

- Good should not have prestige value

- No change in government policy Etc.

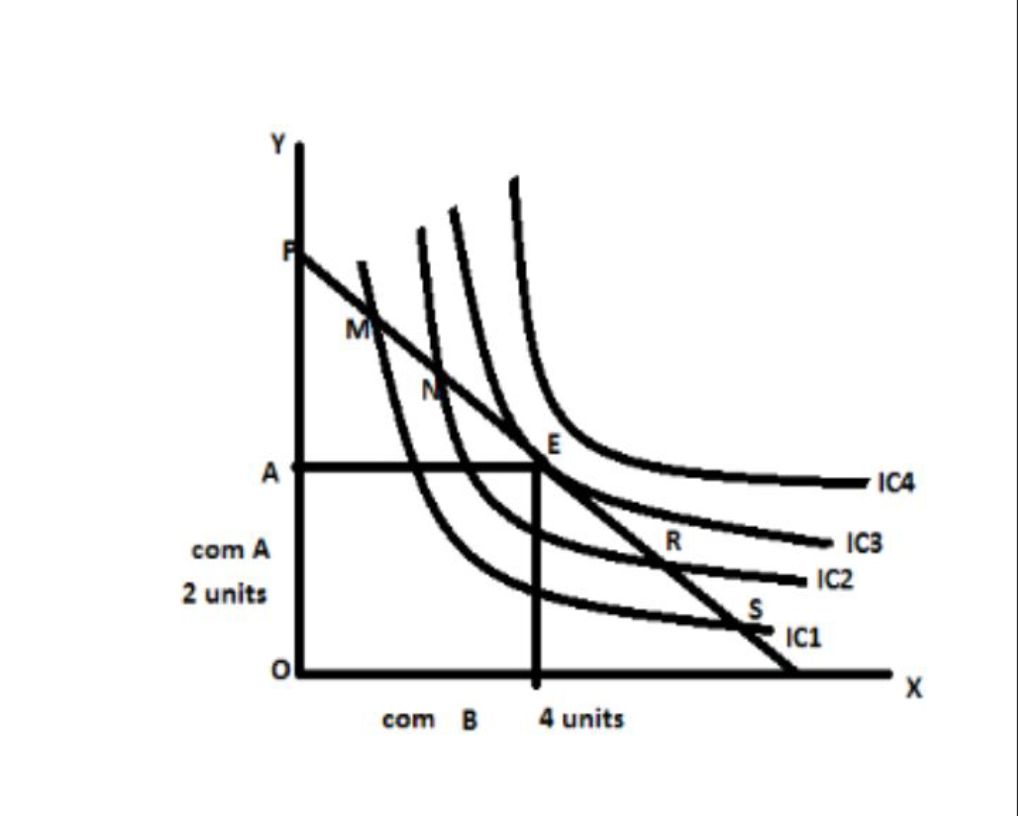

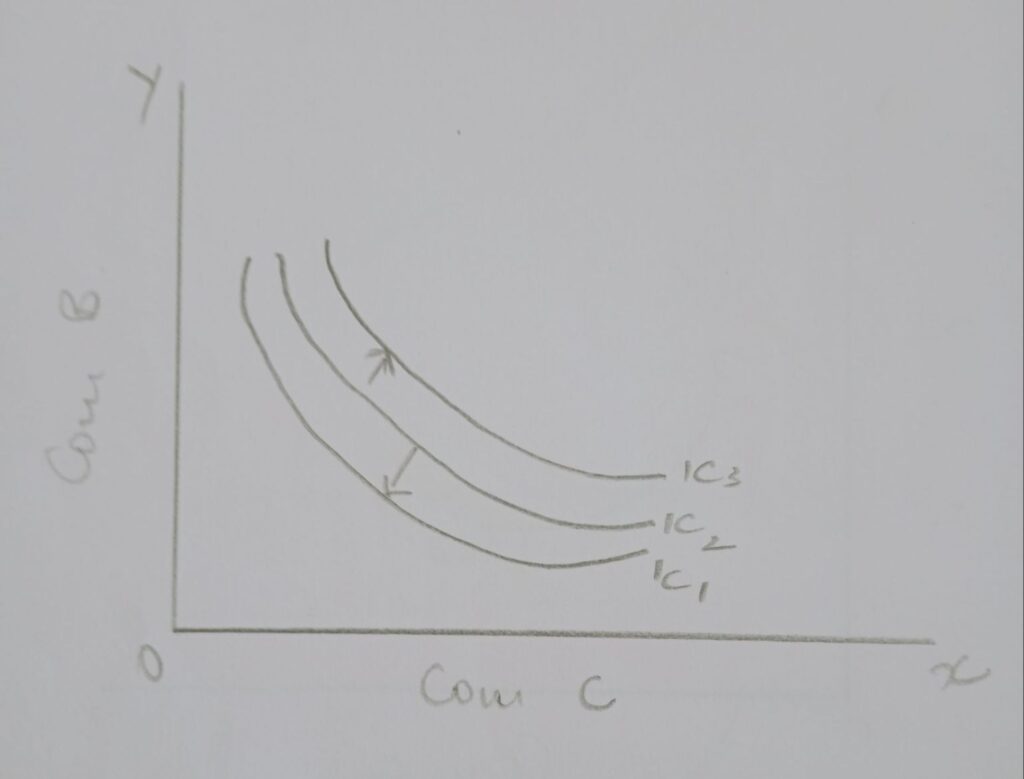

Q. 2. Explain the theory of Consumers equilibrium under indifferent analysis.

The basic objective of the consumer is to drive highest level of satisfaction of a given amount of money in order to achieve this objective; he will spend his limited income in combination of two commodities which will highest told level of satisfaction. The consumer reaches the position of equilibrium when he enjoys the highest level of satisfaction by consuming the most ideal or best possible combination of two goods for a given amount of income. The position of equilibrium will be in the indicate by the point at which the budget line is tangential to the indifference curve. The explanation of the consumers equilibrium analysis is

Assumptions:

- The consumer is rational in his behavior he seeks to maximize his level of satisfaction from the purchase of two goods.

- The consumer has a fixed amount of money income to spend on the two goods A and B.

- Price of two goods is given and constant.

- the consumer will work out possible combination of two goods on the basis scale of preference which would remain unchanged throughout our analysis

- there is no change in taste and habit of the consumer

- Different units of the commodities A and B are homogeneous and divisible and the consumers can conveniently workout different combination of these two goods.

Explanation:

In order to explain the equilibrium of the consumer, we make us of two tools of ICA that is budget line and indifference map.

Illustration

- Income of the consumer is rupees 4,

- price of the commodity A per unit is 25 Paisa and

- Price of the commodity B per unit is 50 paisa.

Assuming that the given income of rupees 4 is spend on commodity A. the consumer get 16 unit of A. similarly assuming that the same income of rupees 4 is spend on commodity B. the consumer can get 8 units of B. when the consumers spends his entire income of rupees 4 on commodity A he get 16 units of A, similarly when he is spend his entire income on B he gets 8 units of B.

The budget line indicates the limited or given income of the consumer with the help of which we can buy a particular combination of two goods A and B. the indifference map represent as subjective scale of preference of the consumer based on his taste, habits and likes and dislikes. it is clear that both budget line and difference map are quite independent of one another in order to explain the equilibrium position of the consumer we have to super imposed the budget line upon the consumer indifference map.

In the diagram, the indifference curve number 3 is meeting the PQ at E. hence PQ budget line is tangent to indifference curve 3 at E. the point of equilibrium.

SHORT NOTES:

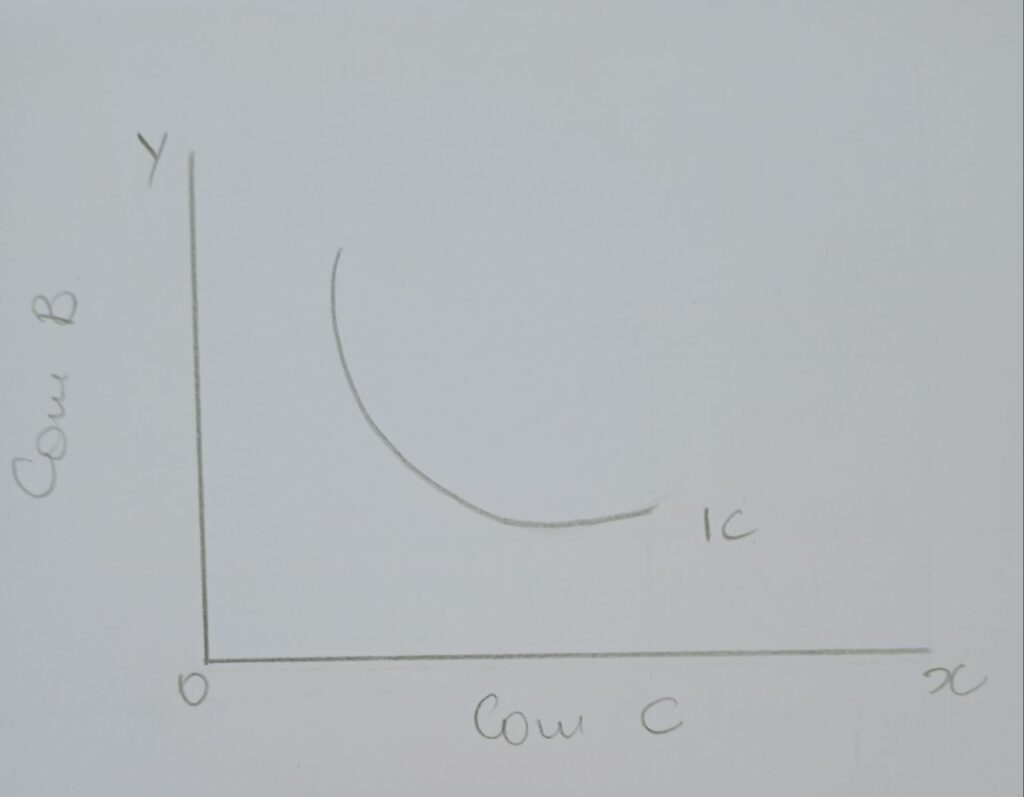

- Properties of Indifference curves:

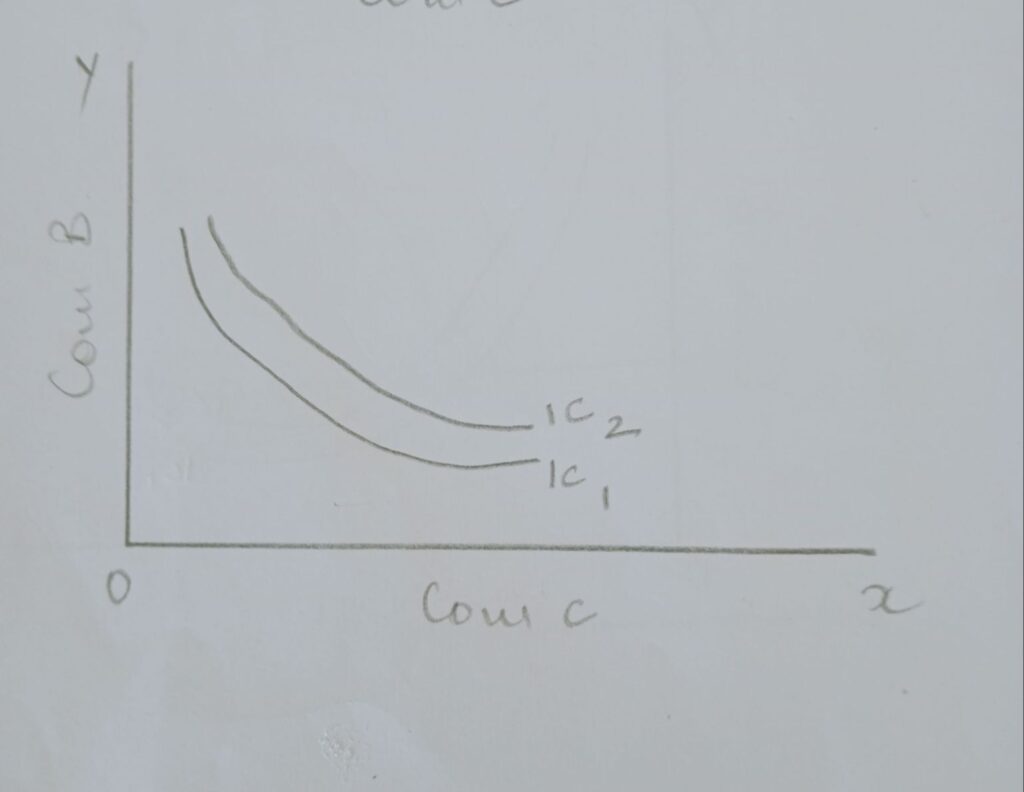

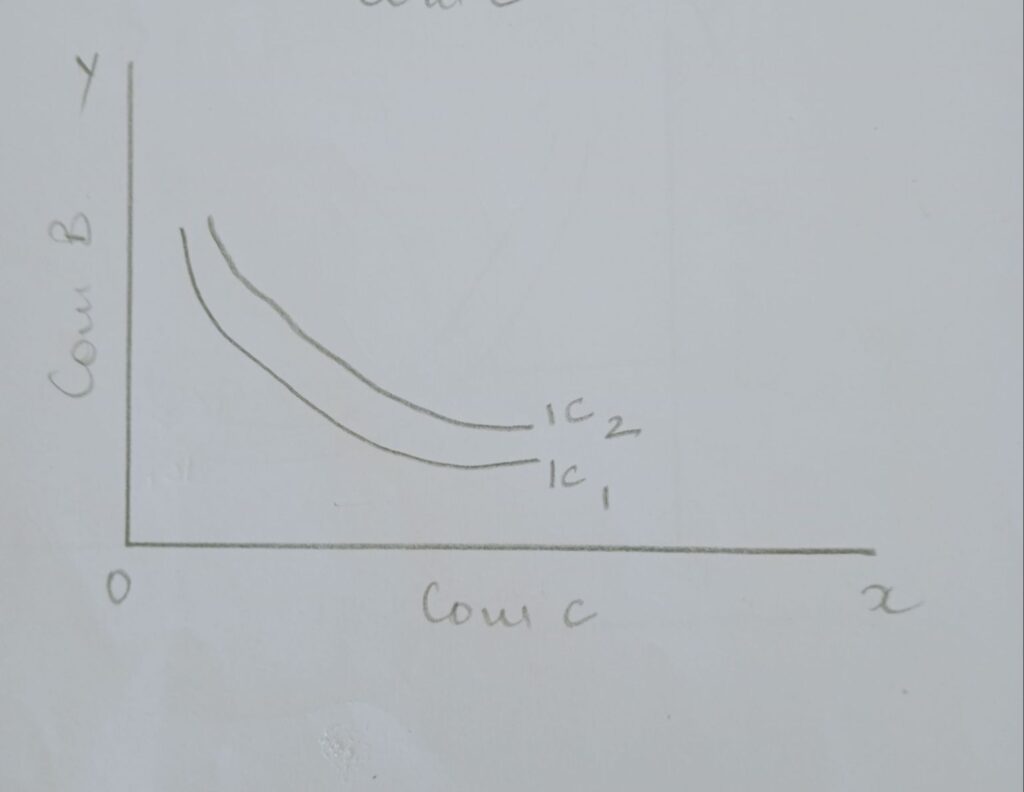

In economics, an indifference curve represents a graphical representation of combinations of two goods that provide a consumer with equal levels of satisfaction or utility. Indifference curves are used in microeconomics to illustrate consumer preferences and choices in decision-making. An indifference curve may be defined as a locus or path indicating different combination of two commodities which yield equal or same level of satisfaction. Properties of indifferent curves indicates the level of satisfaction gets by a consumer from different goods.

According to J R Hicks, “it is the locus of the points representing parts of quantities between which the individual is indifferent and so it is termed as an indifference curve.”

Properties of indifference curve:

- An indifference curve always slope downwards from left to right: In order to represent fall in the quantity of one commodity and increase in the quantity of another commodity, the Indifference curve must slope downwards from left to right. The Indifference curve cannot be moving upward neither horizontal nor vertical line.

- An indifference curve is convex to the origin of the axis: This property is derived from the law of DMRS. The IC always must be convex to the origin of the axis. If the curve is concave in that case DMRS cannot be represented.

- No two indifference curve intersects each other: Each IC represent only one particular level of satisfaction. If two curves cut each other at one point, it indicates equal level of satisfaction at the interesting point . This is against the rule of indifference curve analysis.

- An indifference curve bearing higher number represent higher level of satisfaction and a lower number represent a lower level of satisfaction: Higher IC represents higher level of satisfaction. A consumer moves on from one IC to other, a lower to the higher as his income increases in his income, as he would be able to buy larger quantities of both the commodities, his level of satisfaction increases.

- An indifference curve should touch either of the axis: If the IC touches x axis, it indicates that the consumer is buying only commodity A and if the IC touches Y axis it indicates that he is buying only commodity B at the point where it touches the axis. Hence to represent the combination of two commodities, an IC should not touch either X axis or Y axis.

- Indifference curve are parallel to each other but it is not a rule: Generally speaking they slope downwards and they are parallel to each other .but the rate of substitution between the two commodities may not be the same in case of all IC. it depends on changing economic position of a consumer, there is no definite proportion between the ranges of different levels of satisfaction representing different IC. Hence they may be parallel or may not be parallel as the situation may be.

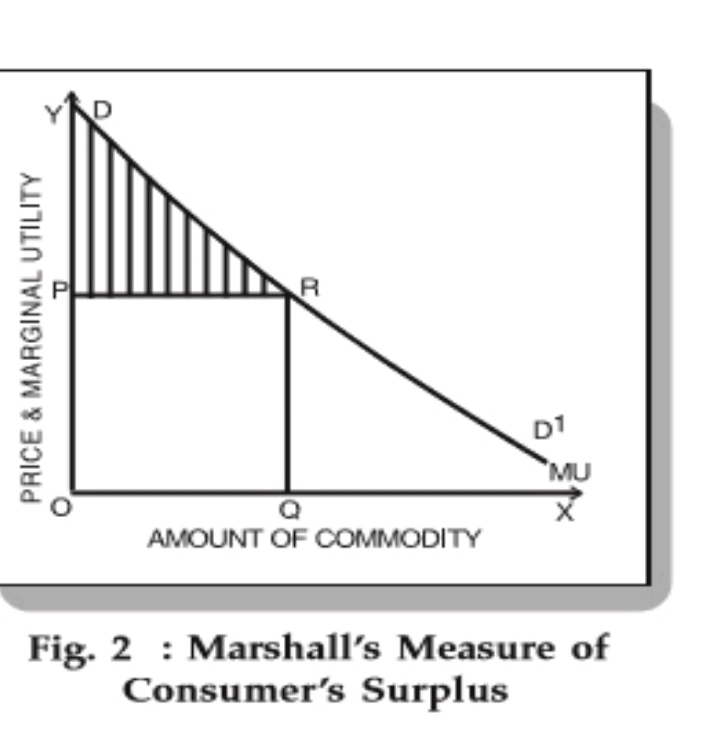

2. Consumers Surplus:

The concept of Consumer’s Surplus was first invented by a French economist Dupuit in 1844. Later it was popularized by Prof. Alfred Marshall in 1980. Because of this consumer’s surplus is also called as Marshallian concept. The characteristics of consumers surplus are also called features.

In a monetary economy, we measure the utility of a commodity with the help of price. The price we pay for a commodity depends on its utility. If commodity possesses higher utility, then it commands higher prices and vice- versa.

The law of EMU states that the price paid for a commodity should be equal to its marginal utility. This is a basic condition for consumer’s equilibrium. At the point if equilibrium neither there will be higher utility nor lower utility. But MU=Price.

In real life a consumer may not act according to the law. The balance between the price and utility may not be maintained always. Sometimes he may get lower utility or higher utility from the commodity when compared to the price he is paying for it. The excess or surplus satisfaction enjoyed by a consumer over and above the price he is paying for a product rather than go without it is called as consumer’s surplus. It is found in the purchase of useful commodities like salt, matchbox, newspaper, and many other such durable and non-durable commodities.

According to Bilas, the difference between what the consumers does to pay for the commodity and what he would be willing to pay rather than go without it is called consumers surplus.

According to Prof. Taussing, consumer’s surplus is the difference between the potential price and actual price. It can be explain with the help of a simple formula.

Consumer’s Surplus= what we are prepared to pay – What we actually pay.

It is noted that there is an inverse relationship between price and consumer surplus. If price rises, consumer’s surplus falls and vice-versa. Consumer’s surplus is a product of opportunities and environment.

The concept of consumer’s surplus can be explained with the help of a table.

| Units of the commodities | M.U. of a commodity | Price per | Consumer’s Surplus in |

| 1 | 40 | 20 | 20 |

| 2 | 35 | 20 | 15 |

| 3 | 30 | 20 | 10 |

| 4 | 25 | 20 | 5 |

| 5 | 20 | 20 | nil |

| Total units | Total utility | Total Price | Consumer’s surplus |

Consumer’s Surplus= Total Utility- [price x Quantity]

Symbolically C.S. = TU-[PXQ]

= 150-[20X5]

=150-100=50

Thus the CS= what we are prepared to pay – what we actually pay.

CS = 200 – 150 =50.

Consumer surplus is a concept in economics that represents the difference between what consumers are willing to pay for a good or service and what they actually pay. It is essentially the surplus or benefit that consumers receive when they can purchase a product at a price lower than the maximum price they are willing to pay.

UNIT-3

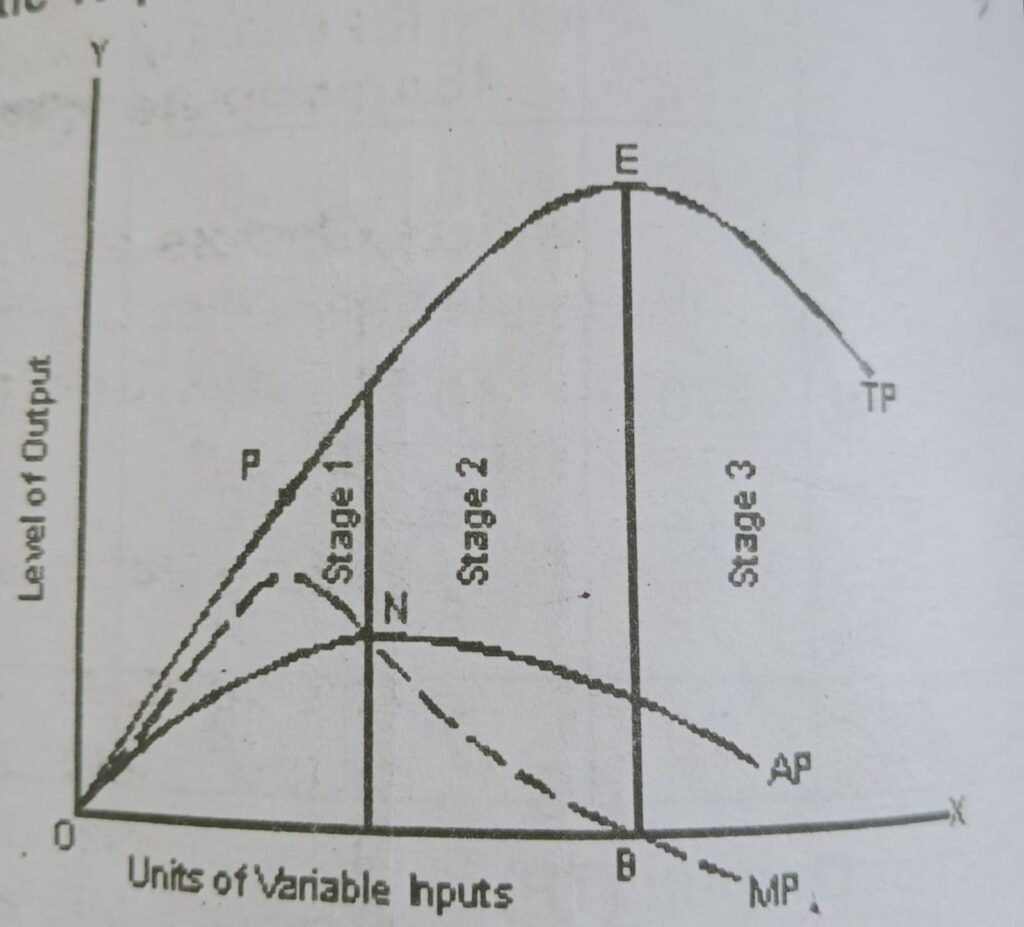

Q. 1. Explain the law of Variable proportions.

In economic theory, the law of variable proportion occupies an vital place. It is one of the fundamental laws of production. The law of variable proportion is the new name for the well known” law of Diminishing returns.” of classical economist. According to classical economists there were three separate laws of production but the modern economist are of the view that these laws are not really separate laws but only three faces of general law of variable proportion. The stages of the law of variable proportion are of three kinds which is based on production.

It explains the input output relation in a situation when the output is increased by increasing the quantity of one input and keeping the other inputs constant. The law explains the relationship between inputs and output in the short period. It explains how the output increases when one factor of production increased, keeping the other factors of production constant, in the short period.

Assumptions of the law:

- It is assumed that one factor unit to be varied and all other factors should kept constant.

- It is based upon the possibility of varying proportions of factor inputs.

- It is assume that all the units of the variable factors are homogeneous and equally efficient.

- Plant size and capacity should remain constant.

- It assumes that the techniques of production remain constant.

STAGES OF THE LAW

The Law of Variable Proportions, or the Law of Diminishing Marginal Returns, is often described in terms of three distinct stages as more of a variable input is added while keeping other inputs constant. These stages are:

- Stage of Increasing Returns: In this stage, the marginal product of the variable input is increasing. Each additional unit of the variable input contributes more to total output than the previous unit did. This stage occurs when there are underutilized resources or when the fixed factors of production are not fully utilized. As more of the variable input is added, specialization and division of labor lead to increased efficiency and productivity.

- Stage of Diminishing Returns: In this stage, the marginal product of the variable input begins to decrease. Although total output continues to increase, it does so at a decreasing rate. This occurs because the fixed factors of production become more intensively utilized relative to the variable input. Additionally, as more units of the variable input are added, factors such as crowding or diminishing returns to specialization start to set in, reducing the efficiency gains.

- Stage of Negative Returns: In this final stage, the marginal product of the variable input becomes negative. This means that each additional unit of the variable input actually reduces total output. This occurs when the fixed factors of production are overused by the variable input. For example, adding too many workers to a fixed amount of capital in a factory may lead to congestion, inefficiency, and ultimately a decline in output.

REASONS FOR THE STAGES.

The stages of the Law of Variable Proportions, also known as the Law of Diminishing Marginal Returns, can be attributed to several reasons related to the nature of production processes and resource utilization. Here are some of the important reasons for each stage:

- Stage of Increasing Returns: Underutilization of Fixed Inputs: Initially, when a variable input is added to a fixed set of inputs, there may be underutilization of the fixed inputs. This means that the fixed inputs, such as capital or land, are not fully utilized, and adding more of the variable input allows for better utilization of these fixed inputs.

- Stage of Diminishing Returns:

- Fixed Input Constraints: As more of the variable input is added, the fixed inputs become relatively more constrained. This means that there is a limit to how much additional output can be produced by adding more of the variable input while keeping the fixed inputs constant. This leads to diminishing marginal returns as the fixed inputs cannot support unlimited increases in the variable input.

- Diseconomies of Scale: Beyond a certain point, adding more units of the variable input may lead to inefficiencies and diseconomies of scale. Factors such as overcrowding, coordination problems, and communication difficulties may arise, reducing the overall productivity of the production process.

- Stage of Negative Returns:

- Overutilization of Fixed Inputs: In this stage, the fixed inputs become overwhelmed by the variable input. There may be physical limitations or constraints on the fixed inputs that prevent them from accommodating additional units of the variable input. As a result, the marginal product of the variable input becomes negative, leading to a decline in total output.

- Congestion and Diminished Efficiency: Adding too many units of the variable input can lead to congestion, overcrowding, and inefficiencies in the production process. Workers may get in each other’s way, leading to reduced productivity and output.

- Specialization and Division of Labor: Adding more units of a variable input often leads to specialization and division of labor, which can increase overall productivity. As workers specialize in specific tasks, they become more efficient at performing those tasks, leading to increasing returns.

Q.2. Explain the properties of capital and organization.

In ordinary the term capital means cash or money, but in economics capital does not means only cash it means wealth that is used for producing additional wealth in other what it refer to all manmade wealth .It includes cash, raw material, tools implements, machines, vehicle, furniture, building etc. The properties of capital are like passive factor, manmade, destructive etc.

Properties of capital:

- Productive: Capital is productive because it helps in production of wealth and goods.

- Produced means: Capital is not an original factor of production as land it is produced means of factors of production it is a product of land and labor.

- Source of Capital: Capital is a source of income it has revenue yielding capacities separable and mobile: capital can be separated from its owner and capital is mobile because it moves easily from one place to another.

- Destructive: Capital is destructive as it can be exhausted or used up.

- Variable: Capital is variable in other words the amount of capital can be increased or decrease.

- Passive factor of production: Capital is a passive of production because it cannot produce anything on its own.

- Stored up labor: Capital is stored up labor when a man earns by putting his efforts and saves a part of his earnings. The saving when invested becomes capital. That means a part of earnings of labor becomes capital or can say that capital is stored by labor.

- Capital depreciates and appreciates: Capital differentiates that is the value of capital example: capital goods like machinery depreciates on account of successive use. Capital is also subject to appreciation for example; gold.

- Capital entails cost: Capital entails cost as capital is a produced factor in entails cost both economic cost and social cost. That is payment for the factors of production and pain, loss of health Etc. involved in earning income and saving.

- Manmade: Capital is known for passive factor made by man, use by man and destroy by man.

Meaning of Organization:

Land, labor and capital cannot produce anything unless they are brought together in a proper proportion and make to work homogeneously. The work of bringing together these three factors of fraction in proper proportion making them works harmoniously. So as to obtain the best result is called organization or entrepreneur. This is clear from the definition of organization given by Haney; according to him organization is a harmonious adjustment of specialized parts for accomplishment of some common purpose or purposes.

Properties of organization:

- Planning: the primary task of an entrepreneur is to plan that is to decide all the aspects of production beforehand. He must decide in an advance the product is to be produced, a quality to be produced, the place of production and the time of production, the technique of production etc.

- Starting: after all the details of production are decrease the entrepreneur must make the necessary arrangement for starting the production he much raise the necessary capital required, construct a factory building, installed the machinery buy required raw material, employee the required labor and start the production.

- Management and supervision: when the production is being carried on the entrepreneur must attend the management and supervisor problem. he must introduced proper division of labor and distribute the work in such a manner that right man is employed for the right place supervision for men and material and ensure that there is no wastage of time, labor, materials

- Marketing: after the production is complete the entrepreneur must make arrangement for the efficient marketing and distribution of his product at the best market. That is at the market where he can get the highest possible price for his product. For this purpose he must established contacts with middleman such as wholesalers and retailer or established his own retail shop make, proper transportation arrangement for the movement of goods and arrange for the advertisement of the product. Further he must study the changing market condition and make suitable changes in market and distribution techniques.

- Innovation: according to Schumpeter, “an entrepreneur is a greater innovator and a leader in breaking the traditional pattern in production” this statement means that an entrepreneur must introduce innovation.

SHORT NOTES:

- Production function:

The term production means transformation of physical inputs in to physical outputs. The term inputs refers to all those things which are required by the firm to produce a particular product. In addition to four factors of production, inputs also include other items like raw materials of all kinds, power, fuel and services like transport and communications, warehousing, banking, shipping and insurance. Thus the term inputs has a wider meaning in economics. What we get at the end of the process is called as output. It refers to finished products. The production function is imported from mathematics.

PRODUCTION FUNCTION.

A production function is used in economics to present the relationship between the factor inputs and outputs in the process of production . It provides a mathematical or graphical representation of how various inputs, such as labor and capital, combine to produce goods and services. The production function is a fundamental concept in the field of microeconomics and is often used to analyze and understand the efficiency and productivity of a firm or an economy.

The general form of a production function is expressed as follows:

Q=f(L,K,…)

Where:

Q is the quantity of output produced.

L represents the quantity of labor input.

K represents the quantity of capital input.

The production function illustrates how the various inputs combine to produce a certain level of output. The function can take different forms, and the choice of the specific function depends on the characteristics of the production process being analyzed. Production function differs firm to firm. It influences number of factors like, the size of resources, the pattern of technology, the firm size, prices of factor inputs Etc.

The nature of production function depends upon the time period allowed for adjustment of inputs. Normally we consider two time period that is short run and long run. Short run refers to the time the period over which amount of some factors called fixed factors cannot be changed. Hence output is changed by using the fixed factors more intensively. long run refers to the time period during which all the factors of production can be changed.

Features of production function:

The features of production includes various aspects that characterize the process of creating goods and services. These features contribute to the efficiency, effectiveness, and overall success of production activities. Here are some key features of production.

1. Creation of Value: The purpose of production is to add value to inputs, making them more useful or desirable. This can involve manufacturing tangible products, providing services, or a combination of both.

2. Economic Activity: Production is a fundamental economic activity and a key driver of economic growth. It contributes to the creation of wealth, employment, and the overall well-being of societies.

3. Stages of Production: The production process often consists of multiple stages, from the initial design or planning phase to the actual manufacturing or service delivery, and finally, distribution to consumers.

4. Efficiency and Optimization: Successful production involves optimizing resources to achieve efficiency, minimize costs, and maximize output. This may include the implementation of technologies, quality control measures, and streamlined processes.

2. Economies of Scale:

Economies of scale refer to the cost advantages that a business or organization can achieve as a result of an increase in the scale of production or size of operations. In other words, as the quantity of goods or services produced or the scale of operations expands, the average cost per unit decreases. This phenomenon is often associated with the efficiency gains and cost savings that come from producing on a larger scale.

ECONOMIES OF SCALE:

Internal economies of scale:

Internal economies of scale refer to the cost advantages and efficiencies that arise within a firm or organization as a result of its own growth and expansion. These economies of scale are specific to the internal operations and structure of the firm, and they can contribute to lower average costs per unit of production as the firm increases its scale of operations. Internal economies of scale can manifest in various ways within a company. Here are some common types:

- Technical Economies: Larger-scale operations often allow firms to invest in and adopt advanced technologies. This can lead to improved production processes, automation, and increased efficiency .Eg. A manufacturing company investing in state-of-the-art machinery that can produce goods at a faster rate and with fewer defects.

- Managerial Economies: As a firm grows, it can benefit from specialized managerial roles, more efficient decision-making processes, and better coordination. Specialization and efficient management can contribute to cost savings. Larger firms may have specialized managers for different functions (production, marketing, finance), leading to more effective decision-making.

- Financial Economies: Larger firms often enjoy better access to financial markets, lower interest rates on loans, and improved terms for financial transactions. E.g. A large corporation may be able to negotiate more favorable terms with banks, obtain lower interest rates on loans, and issue bonds at lower costs.

- Marketing Economies: Larger firms can spread their marketing costs over a larger volume of production, leading to lower per-unit marketing expenses. E.g. A company with a national or international presence can promote its products to a wider audience at a relatively lower cost per customer.

- Purchasing Economies: Larger firms can negotiate bulk discounts with suppliers due to higher order quantities. This results in lower costs for raw materials and components. E.g. A retail chain purchasing inventory in large quantities, negotiating lower prices from suppliers, and benefiting from economies of scale in purchasing.

- Risk-Bearing Economies: Larger firms with diverse operations and a broad product or service portfolio may be better able to absorb and manage risks. E.g. A diversified conglomerate with business operations in multiple industries may be more resilient to economic downturns affecting specific sectors.

External economies of scale:

External economies of scale refer to the cost advantages and efficiency improvements that arise from the overall growth and development of an entire industry or geographic area, rather than from the expansion of a specific firm. Unlike internal economies of scale, which are specific to an individual company, external economies of scale benefit multiple firms within a particular industry or location. These external economies can lead to lower average costs per unit of production for all firms involved. Here are some common types of external economies of scale:

- Industry Specialization: When multiple firms in an industry cluster together, they can benefit from shared infrastructure, specialized labor pools, and common resources. E.g. A tech hub where multiple software development firms share the same pool of skilled programmers, reducing recruitment costs for each company.

- Shared Infrastructure: Firms in the same industry may share common infrastructure such as transportation networks, utilities, and communication systems, leading to cost savings for all. E.g. Several manufacturing plants located in close proximity, sharing the same transportation and logistics infrastructure, reducing shipping costs.

- Skilled Labor Pool: A concentration of firms in a specific industry or location can attract a skilled labor force with specialized expertise, reducing training costs for individual companies’ .E.g. The presence of numerous pharmaceutical companies in a biotech cluster attracting a pool of highly skilled researchers and scientists.

- Knowledge Spillovers: In the presence of other firms the institutions can facilitate the exchange of knowledge and ideas, leading to innovation and efficiency improvements across the industry. E.g. Research institutions, universities, and technology parks in close proximity fostering knowledge sharing among firms in the same sector.

- Government Support: Government policies and incentives that support an entire industry can lead to external economies of scale. This may include tax breaks, infrastructure development, or industry-specific subsidies. E.g. A government providing tax incentives and grants to encourage the growth of a renewable energy industry.

- Access to Inputs: A concentration of firms in an area can lead to improved access to raw materials, suppliers, and specialized services, resulting in cost savings for all participants. E.g. A jewelry district where multiple jewelers benefit from easy access to suppliers of precious metals and gemstones.

- Network Effects: The overall growth of an industry can create network effects, where the value of products or services increases as the number of users or participants grows: E.g. The software industry benefiting from a larger user base, leading to the development of complementary products and services.

UNIT- 4

Q.1. What is Perfect competition? explain its features.

A market means the whole set of condition under which a commodity is marketed, the extent and nature of competition in selling, the nature and number of buyers, the nature of the commodity that different seller of for etc. The features of perfect market depends on its nature.

Perfect competition:

Meaning: A perfectly competitive market is one in which the number of buyers and sellers are very large. All engaged in buying and selling homogeneous product without any artificial restrictions and processing perfect knowledge of market at a time.

Perfect competition is a market structure in economics where a large number of buyers and sellers participate in the exchange of homogeneous (identical) goods or services. In a perfectly competitive market, no single buyer or seller has the power to influence the market price.

According to Bails, “the perfect competition is characterized by the presence of many firms. They all sell identically the same product. The seller is the price taker.

Features of perfect competition

- Existence of very large number of buyers and sellers: a perfectly competitive market will have a large number of sellers and buyers. Output of a seller will be so small that it is a negligible fraction of the output of the industry. Hence changes in supply made by a particular firm will not affect the total output and price.

- Homogeneous product: different firms constituting the industry produce homogeneous goods. They are identical in character hence no firms can rise its price about the general level.

- Free entry and exit of firms: there is absolute freedom to firms to get in or get out of the industry. If the industry is making profit new firms are attracted into the industry. Conversely firms will quit the industry if there are losses. This results in the realization of normal profit by all firms in the long run.

- Existence of single price: each unit bought and sold in the market commands the same price since products are homogeneous

- Perfect knowledge of the market: all the sellers and buyers will have the perfect knowledge of the market. Sellers cannot influence buyers and buyers cannot influence the sellers.

- Perfect mobility of factors of production: factors of production or free to move into any use or occupation in order to on higher rewards. Similarly, they are also free to come out of the occupation or industry if they feel that they are under remunerated.

- Full and unrestricted competition: perfectly competition market is free from all sorts of monopoly, oligopoly conditions. Since there are very large number of buyers and sellers. It is difficult for them to join together and form other organization. Hence each firms acts independently

- Absence of transport cost: all firms will have equal access to the market, consequently market price change by the sellers does not vary because of differences in the cost of transportation.

- Absence of artificial government control: the government do not normally interfere in the matters pertaining to supply and price. It does not place any banners in the way of smooth exchange. Price of a commodity is determining only by the interaction of supply and demand forces in the market.

- The market price is flexible over a period of time: market price changes only because of changes in either demand or supply force or both. Thus the seller, buyer, industry or the government do not influence price.

Q. 2. What is Monopolistic competition? explain its features.

Professor Chamberlain is the main architect of the theory of monopolistic competition this market exhibition the characteristics of both are competition and monopoly. Since modern markets are combined and integrated with Monopoly powers and competitive forces they are called as monopolistic competition. It is a market structure in which large number of small seller sell differentiated product which are close but not perfect substitutes for one another. The features of monopolistic competition are peculiar.

Monopolistic competition is a market structure in economics that combines elements of both monopoly and perfect competition. In a monopolistic competition market, there are many firms, each producing a differentiated product that is unique in some way, leading to a degree of product differentiation. However, unlike in a monopoly, there is relatively easy entry and exit of firms, and each firm has limited market power.

Features of monopolistic market:

- Existence of large number of firms: under monopolistic competition the number of firms producing a product will be large. The size of each firm is small. No individual firm can influence the market price. Hence each firm will act independently without worrying about a policies followed by other firms. Each firm follows an independent price output policy.

- Market is characterized by imperfections :It may arise due to advertisement differences in transport cost, irrational preference of customers, ignorance about the availability of different brands of product and prices of products Etc .seller may also have inadequate knowledge about market and prices existing at different segments of market.

- Free entrance exit of firms: Each firm produces a very close substitute for the existing brands of a product. The differentiation provides ample opportunity for a firm to enter with the group or industry. On the contrary if the firm faces the problem of product obsolescence, it may be forced to go out of the industry.

- Element of monopoly and competition: Every firm enjoys some sort of monopoly power. But it is neither absolute nor complete because each product faces competition from rival sellers selling different brands of product.

- Similar but not identical product: Under monopolistic competition the firm produces commodities which are similar to one another but not identical or same. For ex: tooth paste, blades, shoes, cigarettes etc

- Non price competition: In this market there will be competition among many competitions for their products and not for the price of the product. thus there is product competition rather than price competition.

- Definite preference of the consumer: Consumer will have definite preference for particular variety or brands loyalty owing to the special features of a product produced by a particular firm.

- Product differentiation: The most outstanding feature of monopolistic competition is product differentiation firms adopt different technique to differentiate their products from one another. It may take only two forms:

- Real product differences

- Imaginary product differences

- Selling cost: There is unique features of monopolistic competition selling cost are present among monopolistic competition because product differentiation is the hallmark of this market condition.

- Price Elastic Demand: The demand for each firm’s product is relatively elastic, meaning that changes in price will have a noticeable impact on the quantity demanded.

- Profit Maximization: Firms aim to maximize their profits by setting prices and output levels. They will produce where marginal cost equals marginal revenue.

- Imperfect Information: Consumers may not have perfect information about all products in the market. Advertising and branding play a role in influencing consumer choices.

SHORT NOTES:

- Price Discrimination:

Generally speaking the monopolist will not change uniform price for all the customers in the market he will follow different methods and the different circumstances. The policy of price discrimination refers to the practice of a seller to change different prices for different customer for the same commodity produced under a single control without corresponding differences in cost. When the Monopoly firm adopts this policy it will become a discriminatory monopoly which is called as types of price discrimination.

Price discrimination is a pricing strategy where a business charges different prices to different customers for the same product or service. This strategy is typically employed to maximize profits by capturing the maximum amount of consumer surplus, which is the difference between what consumers are willing to pay and what they actually pay.

According to professors, monopolist may be able however to divide his sales among the number of different markets and to change a different price in each market.

Types of price discrimination:

Professor AC Pigou speaks of three kinds of price discrimination.

- Discrimination of the first type: Under price discrimination of the first degree the producer exploits the consumer to the maximum possible extent by asking him to pay the maximum price. he is prepared to pay rather than go without the commodity in this case the monopolist will not allow any consumer surplus to the consumer this type of price discrimination is called perfect discrimination. The seller charges each customer the maximum price they are willing to pay. This method is difficult to implement because it requires detailed knowledge of each customer’s willingness to pay.

- Discrimination of the second type: In case of discrimination of the second degree the monopolist charges different prices for different units of the same commodity but not as maximum possible rate but at a lower rate. The monopolies will leave a certain amount of consumer surplus with the consumer this is done to keep the consumers happy and prevent entry of potential rivals. railway companies adopt this method. Prices vary according to the quantity demanded or consumed. Often, customers buying in bulk receive discounts.

- Discrimination of the third type: In case of discrimination of the third degree the markets are divided into many submarkets or subgroups the price charge in each case roughly depends on the ability to pay of different sub group in the market this is the most common type of discrimination followed by monopolist. Different prices are charged to different groups based on their attributes, such as age, location, or income.

2. Duopoly:

Duopoly is that market situation where there are only two firms operating in the market. Since there are only two firms producing identical goods under duopoly any change in price or output by one firm is bound to affect the other. In duopoly the individual firm has to carefully consider the indirect effect of its own decision to change its price or output or both. There are three classical duopoly models given by Court not, Edge worth and Chamberlin. The features of monopoly are very simple.

Many economist are of the opinion that duopoly is only a firm of simple oligopoly. In other words duopoly is only limited oligopoly. Duopoly models and explanation can also be taken as oligopoly models. Duopoly is a market with two sellers exercising control over the supply of commodities it is a two firms industry.

In the words of Cohen and Crete “where there are exactly two sellers in the market, there is a special case of oligopoly called duopoly.” Each seller knows whatever he does will affect his rival policies. Each seller attempts to make a correct guess of his rival motives and actions the action by one will have a reaction from the other.

FEATURES OF DUOPOLY MARKET

A duopoly is a market structure in which there are only two significant competitors or firms that dominate the entire industry. Duopolies are characterized by a strategic interdependence between the two firms, as each firm’s decisions and actions have a direct impact on the other. Here are some features of a duopoly market in economics:

- Two Dominant Firms: A duopoly consists of two main players or firms that dominate the market. These firms have a substantial market share and influence over the industry.

- Strategic Interdependence: The actions and decisions of one firm directly affect the other. Firms in a duopoly must consider the potential reactions of their competitor when making strategic choices, such as pricing, production levels, and marketing.

- Limited Competition: Due to the small number of firms, competition is limited compared to more competitive market structures like perfect competition. The behavior of each firm has a significant impact on market outcomes.

- Product Differentiation: While products may be similar, there is often some degree of product differentiation to distinguish one firm’s offerings from the other. This differentiation can be in terms of quality, features, or branding.

- Barriers to Entry: Entry barriers exist, making it difficult for new firms to enter the market and compete with the established duopoly. These barriers may include high startup costs, access to distribution channels, and economies of scale.

- Price Rigidity: Duopoly sellers may engage in price rigidity, where they avoid frequent price changes due to the potential for retaliation by the other firm. This can lead to price stability in the market.

- Collusive Behavior: Firms in a duopoly may engage in collusion, where they coordinate their actions to maximize joint profits. Collusion can take the form of price-fixing, output restrictions, or other cooperative agreements.

- Non-Price Competition: Competition may extend beyond prices, with firms focusing on non-price factors such as product quality, advertising, and customer service to gain a competitive edge.

- Oligopolistic Tendencies: Duopolies share some characteristics with oligopolies, which are markets dominated by a small number of large firms. However, the distinction lies in the specific number of firms involved.

- Game Theory Application: Game theory is often applied in the analysis of duopolies to understand the strategic interactions between the two firms and predict their likely behavior.

UNIT-5

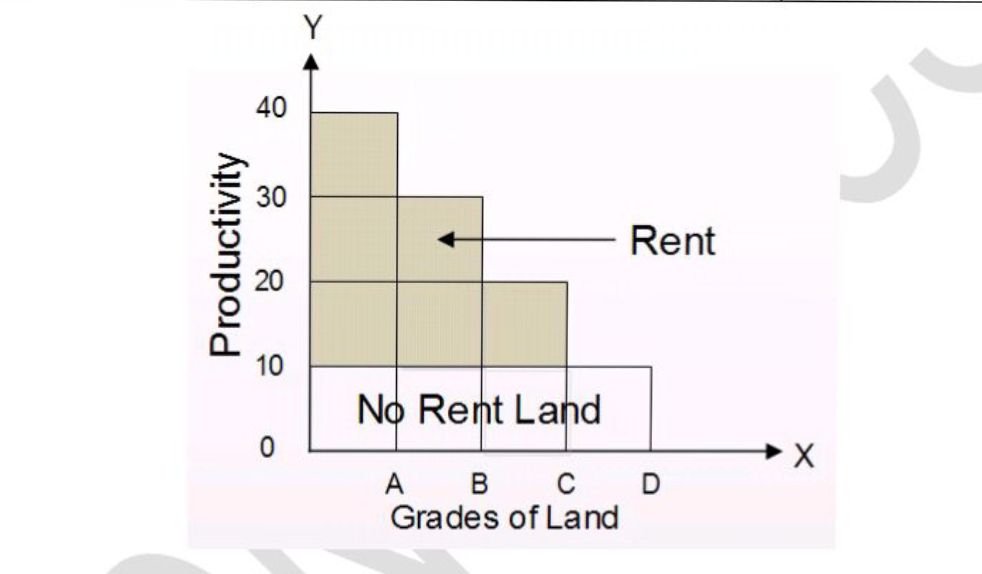

Q.1. Explain the Ricardian theory of Rent.

In the ordinary language, the term rent means any periodical payment made by a person for the privilege of using an asset belonging to someone else. It denotes a payment made for the hiring of a particular thing such as a house, car machine Etc. all these are the instance of periodic payment and call the contractual rent. The Ricardian Theory of Rent is also called as classical theory of rent.

But in economics the term rent is used in a special sense. It refers only to the income received from the ownership of land or other free gifts of nature. It is a reward for the service of land in the process of production.

Ricardian Theory of Rent:

Ricardo was the first person who formulated a comprehensive theory of rent. He defined rent as “the portion of the produce of the earth which is paid to the landlord for the use of original and indestructible powers of the soil”

According to Ricardian definition, rent is the payment for the use of land only and differs from contractual rent which includes the return on capital investment made by the landlord. When return on capital investment is deducted from the contractual rent what is left is pure land rent.

Assumption:

- The supply of land from the point of view of the entire society is assumed to be fixed. That is the total supply of land is taken as perfectly inelastic.

- Ricardo assumes that land can be used for the production of only one crop he ignores that land can put to various alternative uses.

- He defines that land differs in quality. Some pieces of land are more fertile than others or may be located nearer to the market.

- The theory assumes that various pieces of land are cultivated in the declining order of their fertility.

- The theory based on the assumptions of the law diminishing return in agriculture.

- The theory assumes that there is no rent on marginal land

- The theory is based on the assumption of long run

Explanation of the Ricardian theory: According to this theory, the cause for the emergence of rent is the difference in the fertility of land the more fertile land would be cultivated first followed by the next best superior land. The output produced by the most appears land is more than the output produced by the next superior land. The difference of the produce of the first category of land that of second category of land is called rent. As successive inferior land are cultivated rent start emerging on the superior land this further increase the rent on the superior land.

Suppose A B C and D is four pieces of land in the order of fertility. so quintals of rice are produced by cultivated land A. as the population increases land B is also cultivated which is inferior to land A as regards to fertility and produce from this land is 60 quintals now land A generates a rent of 20 quintals (80-60=20) as population increases further land c and d are also cultivated and they produce 40 and 20 quintals respectively now the land D is marginal land and therefore full land B generates rent of 60 quintals land B generates rent of 40 quintals and land C 20 quintals this can be shown with the help of the following table and graph.

| Type of land | Produce of rice (quintals) | Rent (quintals) |

| A | 80 | 80-20=60 |

| B | 60 | 60-20=40 |

| C | 40 | 40-20=20 |

| D | 20 | 20-20=0 |

(note: the above numbers of y axis 10,20,30,40 should actually taken as 20 ,40, 60,80.)

Land D is the marginal land or no rent land. Excess of the portion over the produce of land D is the rent which is indicated by the shaded portion.

Ricardian theory applies to extensive as well as intensive cultivation of land. Under extensive cultivation more and more land is cultivated to produce more. The above example of four type of land is an example relating to extensive cultivation.

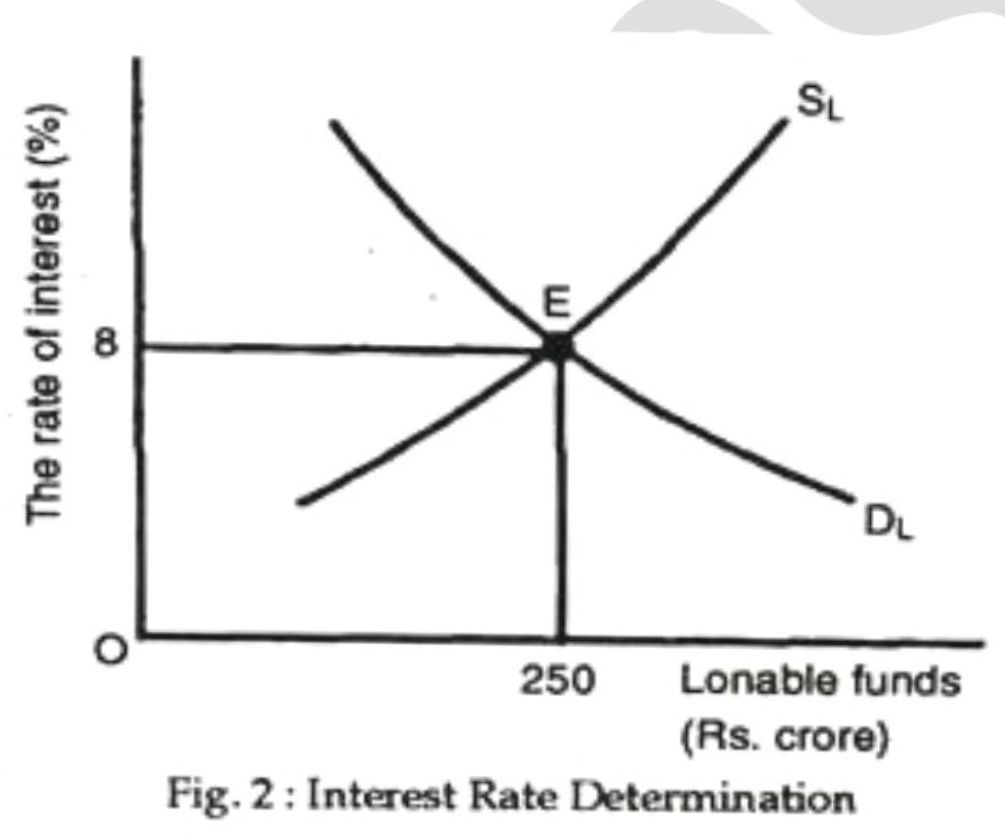

Q. 2. Explain the loanable funds theory of interest.

Loanable funds theory of interest is an extension of the classical theory of interest the theory was formulated by a Swedish economist wick sell. Later on professor Robertson, Ohlin and others have redefined it.

According to the theory the equilibrium interest rate is determined by the equality between demands for supply of loanable funds, interest rate is the price paid for the use of these loanable funds.

Definition:

In the words of Hansen, the interest rate is determined by the interaction of demand schedule for the loanable funds with the supply schedule. The expression loanable fund is wider in its scope. Loanable funds are the sum of money supplied and demanded at any time in the money market.

Loanable Funds Theory of Interest:

Supply of loanable funds:

- Savings: Savings by individuals and household constitute the most important source of supply of loanable funds they are of two types

- Planned or ex-ante savings – Saving planned by individuals at the beginning of a period in the hope of expected incomes and anticipated consumption expenditure.

- Unplanned or ex-post savings: It is the difference between the income of the preceding period and consumption of the present period the level of savings depend on the level of income.

- Dishoarding: Dishoarding of idle cash balances, past savings Etc. may be released into the market dishoarding will be greater if interest rate is high and vice versa.

- Bank credit: As manufacturers of money create credit money and advance it to the individuals and business units generally speaking higher the interest rate higher would be the advances and vice versa.

Demand for loanable funds:

- Demand for investment: loanable funds are demanded for investment purposes. Investment may be undertaken either by individual, business, houses or companies the investment demand depends on the productivity of capital. It is interest elastic it varies inversely with the interest rate lower the interest rate higher would be the demand and vice versa.

- Demand for consumption: people may borrow for consumption purpose it arises when the expenditures are greater than the income of the people. This also varies inversely with the interest rate lower the interest rate higher would be demand for loans and vice versa

- Demand for hoarding: some people may like to hoard a park of their saving in cash. Hoarding implies keeping cash balances this desires to hoard cash is called liquidity preference. It is important to note that some people who are holding cash balance or also the suppliers of loanable funds. The demand for hoarding is interest elastic thus the demand curve slopes downwards from left to right.

SHORT NOTES:

- Wage differentials:

The term wage differential refers to the wage differences which exist between different occupations or different individuals in the same occupation. For example a film star may earn RS 2cr a year which a bank clerk may earn only 1.2 lacs a year, again one film star may earn more than the other film star. This we come across wide differences in the earnings of different persons. The causes for the wage differentials are classified in to demand for and supply of labor.

Causes for wage differentials

- Demand for labor

- Supply of labor

Demand for labor:

- If the demand for any type of labor is high it will command a higher wage and vice versa.

- If the demand for any of labor is in elastic then it will command higher wages and if the demand is elastic it will command lower wages.

- In general wages are equal to the marginal productivity of the labor but it is to be noted that the marginal productivity of labor is different in different occupations depending upon degree of scarcity of each kind of labor in relation to demand for it. Hence wages are born to be different.

- When the economy is growing, businesses expand, leading to an increased demand for labor.

- High consumer demand for goods and services prompts businesses to hire more workers to meet this demand.

- Lower wage rates can increase the demand for labor as it becomes more cost-effective for businesses to hire additional workers.

Supply of labor:

The supply of labor in any particular occupation depends on the following factors;

- Conditions of work: person for employed in agreeable light, clean, fairly comfortable, respectable and pleasant occupation usually get low wages for example clerks, typist, teachers etc are very poorly paid. On the other hand people employed in disagreeable, risky, unpleasant, and dirty and tire some jobs are paid high wages.

- Cost of training: jobs that is more simple easy and cheap to learn carry low wages as against those job which are difficult more expensive and take more time to learn. For example the wages of engineers’, doctors, computer programmers etc higher than those of ordinary and untrained unskilled and inexperience workers.

- Regularity of employment: those jobs that provide a regular and permanent employment throughout the year will be accepted by the people even if the earnings are low on the other hand in case of irregular seasonal and temporary jobs the level of wages high vice versa.

- Degree of fail in confidence and trust: people on whom a greater degree of faith, confidence and trust is to be reposed will on higher wages towards for example goldsmith, jewelers, managers, internal auditors Etc. in such jobs one has to maintain secrecy and high degree of responsibility hence they command high wages

- Dangerous and risky jobs: people who are employed in risky and dangerous jobs receive higher wages than other. For example pilot, workers working in mines etc.

- Natural gifts: there are certain jobs which requires some natural gifts everybody cannot be a successful actor, musician, sport person, artist Etc. since there very small in supply there earnings are very high.

- Intelligence ability talent and knowledge: people with higher level of intelligence, knowledge, talent and abilities will earn much more than ordinary workers. These people come under the “non competing groups”.

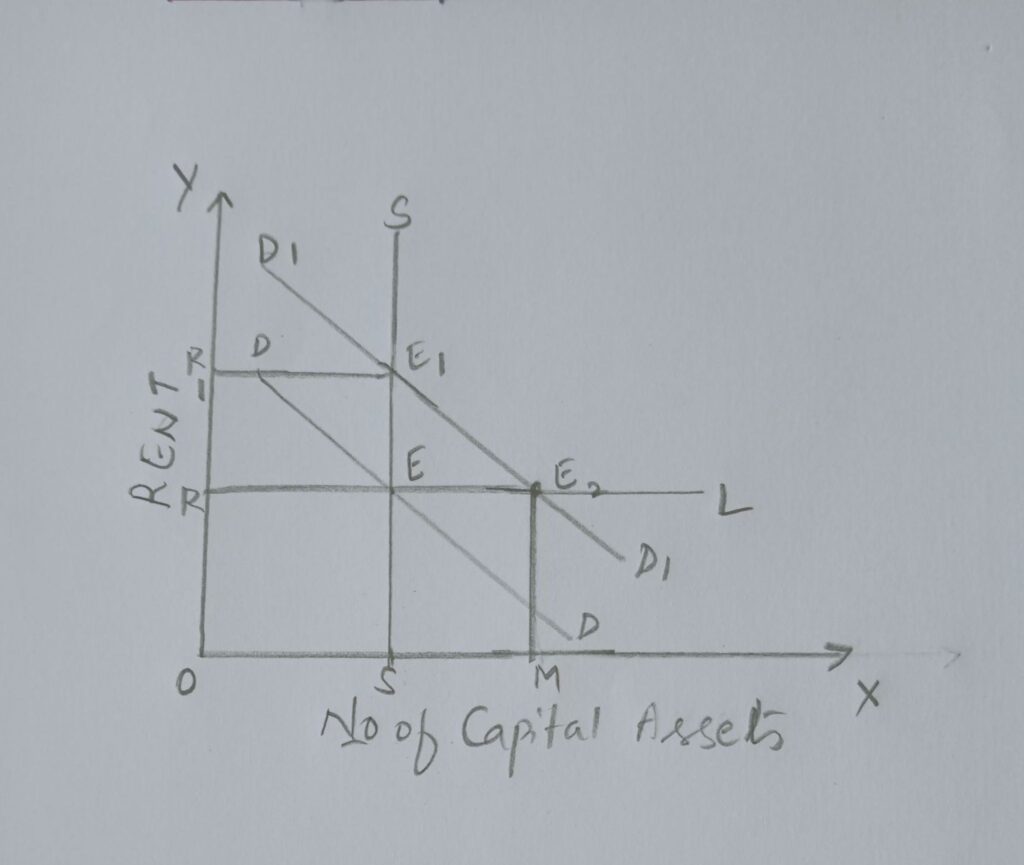

2. Quasi-Rent:

The concept of quasi rent was first introduced by Marshall. He explained that besides land, other factors also get rent the only difference is that rent may accrue to land in the long run also whereas it accrues to others factor only in the short run.

Concept of Quasi-Rent:

Marshall explained that the supply of land is perfectly inelastic and when demand goes up it price also increases and this is called rent. The supply of man made goods and capital is also fixed in the short run. If the demand increases it leads to an increase in the price of such goods and they start getting some surplus over and above the price which they were already getting .this surplus is nothing but quasi rent. it is the economic rent that arises in the case of man made goods in the short run. In the short run, a firm must get that much price which may cover it AVC. If the price is more than AVC. it means that the minimum price it would likely to get thus the excess price over AVC is economic rent. This is explained with the help of a diagram.

Output is Measures on x axis and the cost and revenue on y axis AVC represent the average variable cost and MC the marginal cost in the short run. MR is the marginal revenue. Assuming it to be a competitive firm, the equilibrium is a point E in the short run. The firm must recover its AVC which is equal to FQ but equilibrium price is EQ and it exceeds AVC by EF amount thus EF is the quasi rent and is the difference between the price and AVC.

Marshall’s analysis of quasi-rent is embedded in his discussion of the short run and long run in the theory of production. In the short run, certain factors of production may be fixed and unable to be adjusted. During this period, if the demand for a product increases, the price and revenue of that product may rise, leading to what Marshall referred to as quasi-rent.

In the long run, all factors of production are considered variable, and the supply of factors can be adjusted to changes in demand. In this context, quasi-rent disappears as factors of production can be reallocated or expanded in response to changes in market conditions. In the long run there is adequate time to increase the production and supply of capital assets when demand for them rises. Consequently, the prices of these will come down to the original price level. The short run surplus thus disappears. in the long run total revenue equals total costs. Hence there will be no surplus. It is clear from the diagram.

Marshall’s treatment of quasi-rent may not be as explicit or formalized as in the works of other economists like David Ricardo, his ideas on short-run and long-run adjustments laid the foundation for understanding how returns to factors of production can be influenced by changes in demand and supply conditions over time.

also refer: ECONOMICS1- ecolaw